I have a somewhat illiquid position but Alpaca is using the bid price instead of the mark price. This is not the case on TradeStations or IBKR or any other platform I have been on. The reason this is important is because it lowers your buying power a lot potentially.

It’s also a problem since my application integration uses mark pricing (as it should).

@tuck Where are you seeing “Alpaca is using the bid price instead of the mark price?” Also, by “mark price” are you meaning the latest trade price?

The market data APIs return both the quotes and the latest prices. The trading APIs (eg the /positions endpoint) calculate prices P/L etc based upon latest trade price and not quotes. For example

# fetch current portfolio holdings

GET \https://paper-api.alpaca.markets/v2/positions \

# returns objects like this

{

"asset_id": "79626cfb-3453-4480-8498-85f934b390b9",

"symbol": "BCI",

"exchange": "ARCA",

"asset_class": "us_equity",

"asset_marginable": true,

"qty": "731.298556124",

"avg_entry_price": "21.47",

"side": "long",

"market_value": "16161.69809", # this is qty x current_price

"cost_basis": "15700.98",

"unrealized_pl": "460.71809", # this is market_value-cost_basis

"unrealized_plpc": "0.0293432696557794",

"unrealized_intraday_pl": "0",

"unrealized_intraday_plpc": "0",

"current_price": "22.1", # this is the last traded price (ie not quote)

"lastday_price": "22.1",

"change_today": "0",

"qty_available": "731.298556124"

},

Are you perhaps asking why Alpaca uses the bid price when simulating sells in paper trading? If so, the answer is simple. That is typically what market orders will fill at in live trading. Why? NBBO (ie National Best Bid Offer) quotes, as the name implies, are the current best displayed prices anyone is willing to buy or sell for. The bid is the highest anyone is currently willing to buy for. The ask is the lowest anyone is willing to accept to sell. Market buy orders then fill at the bid which is the most anyone is willing to pay at that moment. There are subtleties, but that’s the gist. Paper trading simulates live trading quite well.

If that’s not what you were asking reply back. Perhaps with an example.

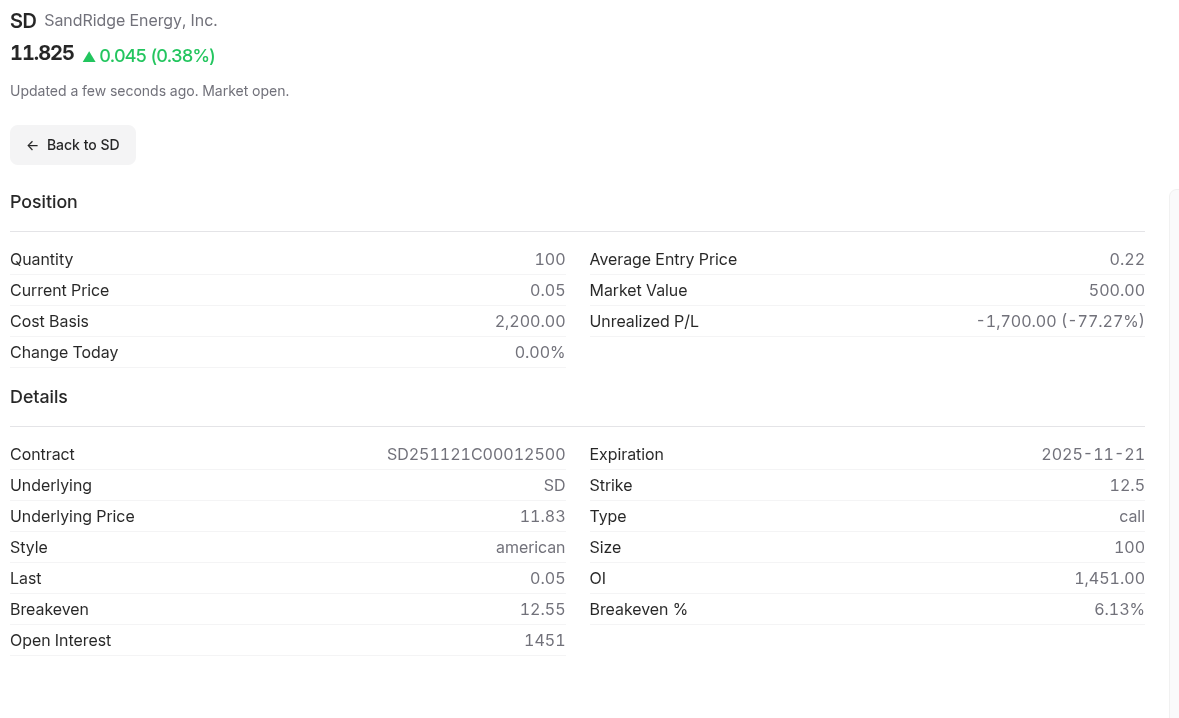

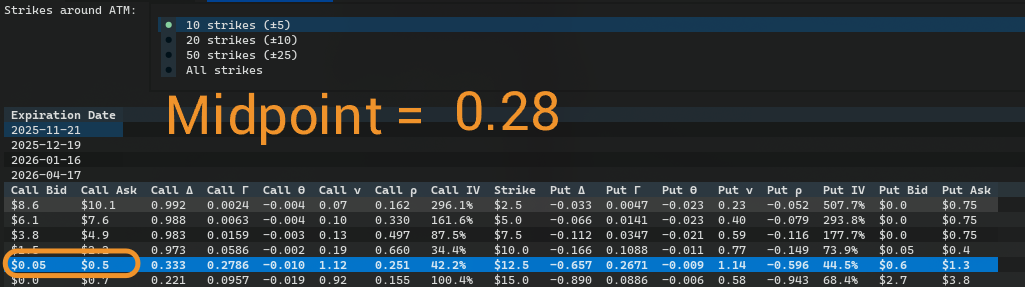

However the bid/ask midpoint is 0.28. I understand the spread is large however it should go off of the mark/midpoint price. The result of this is lowered buying power.

@tuck As mentioned, the ‘price’ for an option contract held long is the bid price which is the expected price you would get if you sold it. Could you give an example of why you feel this results in lowered buying power.